Here’s a fun exercise for anyone who still believes the stock market is a rational pricing mechanism: go read Alphabet’s fourth-quarter earnings report from February, then check what happened to the stock price afterward.

Go ahead. I’ll wait.

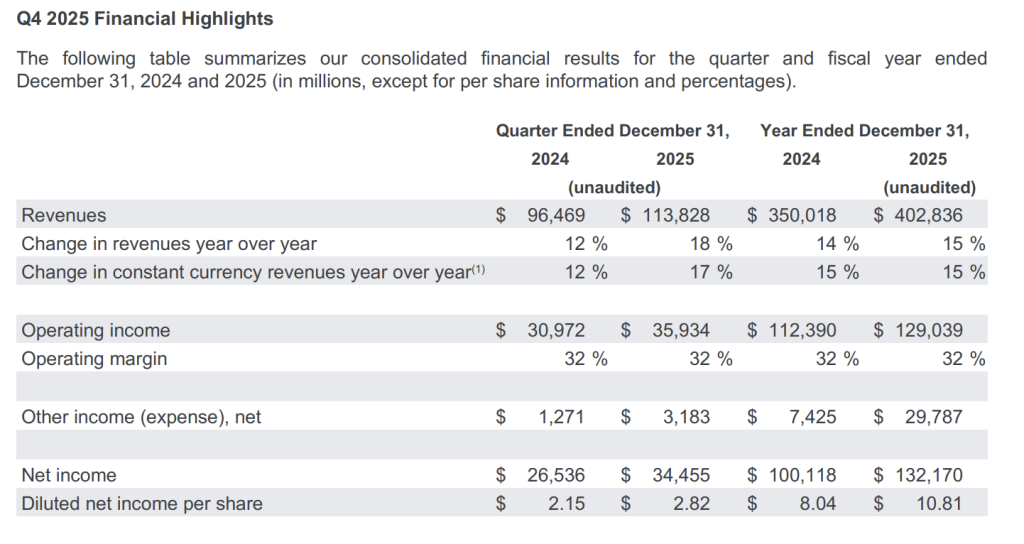

Are you surprised to find that Alphabet posted $113.8 billion in quarterly revenue — up 18% year over year. Net income surged 30% to $34.5 billion. Earnings per share came in at $2.82, crushing the $2.61 Wall Street consensus by 8%. Google Cloud revenues exploded 48% to $17.7 billion. Annual revenue crossed the $400 billion threshold for the first time in the company’s history, and operating cash flow hit a company record of $52.4 billion in a single quarter. By any rational measure, this was a masterclass in corporate execution.

And the stock fell 3% in after-hours trading.

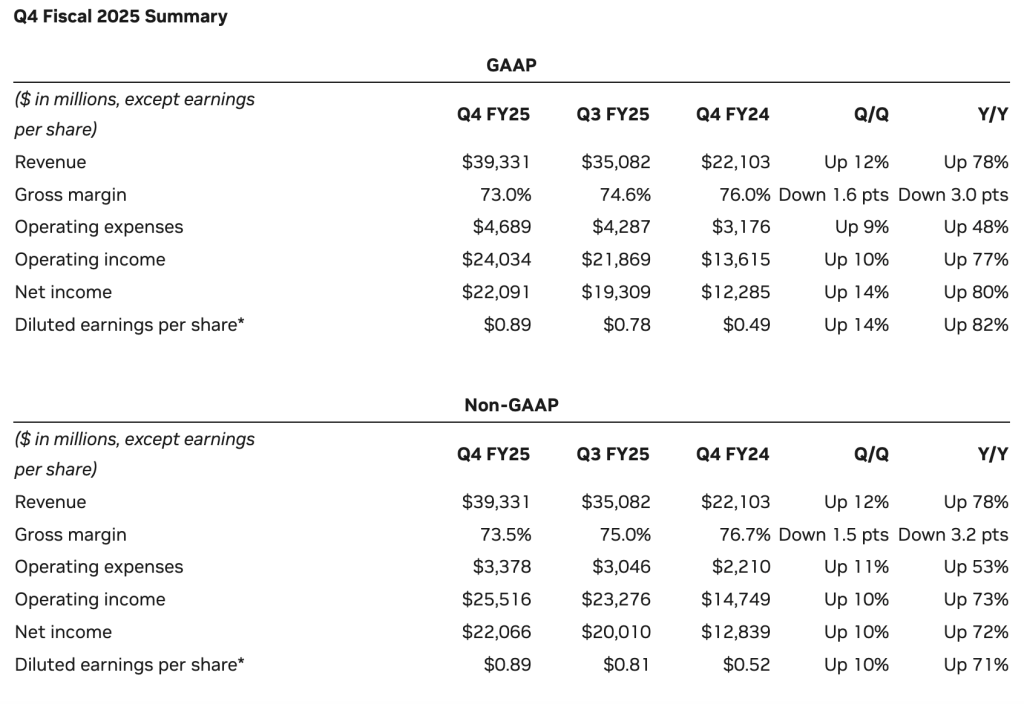

Now do the same exercise with NVIDIA. In late February, the chipmaker reported Q4 fiscal 2026 revenue of $68.1 billion — a 73% surge from the year prior and nearly $2 billion above analyst expectations. Adjusted earnings per share landed at $1.62 versus the $1.53 consensus. Data center revenue, now representing over 91% of total sales, hit $62.3 billion. Net income nearly doubled to $43 billion. The company’s guidance for Q1 fiscal 2027 — $78 billion in projected revenue — exceeded estimates by more than $5 billion, prompting analysts to describe it as having “reset the math” for the entire AI chip cycle.

The stock dropped 5.5% and erased $260 billion in market capitalization overnight.

Welcome to the ball pit. Take off your shoes. The children are already playing.

The Magnificent 7 — Google, Meta, Amazon, Apple, Microsoft, and NVIDIA (we’ll leave Tesla in the corner where it belongs) — are collectively experiencing what can only be described as an epistemological crisis.

Every single one of these stocks is down in 2026. Together, they have shed more than $2 trillion from their peaks. The Roundhill Magnificent Seven ETF has fallen more than 9%, underperforming the broader market. Microsoft alone has cratered 32% in five months.

And yet the fundamentals, as Deepwater Asset Management’s Gene Munster put it bluntly in late March, “have done exceptionally well.” Stocks are simply not reflecting that reality. These companies are reporting double-digit revenue growth, expanding margins, and guiding above consensus estimates. Alphabet is expected to report Q1 2026 EPS of roughly $2.67 when it releases earnings later this month. NVIDIA’s Q1 fiscal 2027 revenue guidance of $78 billion dwarfs the annual revenue of most S&P 500 companies. The four major hyperscalers — Alphabet, Amazon, Microsoft, and Meta — are projected to spend close to $700 billion in capital expenditures this year, a 60% increase from 2025, a staggering vote of confidence in AI’s commercial future.

But none of that seems to matter when the adults leave the room and the institutional traders start throwing balls at each other.

Let’s talk about what actually moves these stocks, because it certainly isn’t earnings reports.

On February 28, 2026, the United States launched military strikes against Iran. Since that day, the S&P 500 has declined roughly 7%. The Dow Jones Industrial Average has shed nearly 4,000 points and officially entered correction territory — down more than 10% from its most recent high. The Nasdaq Composite has plunged over 13% from its October peak. On a single Friday in late March, the Magnificent 7 collectively lost over $330 billion in market capitalization. Over that same week, the group hemorrhaged roughly $870 billion.

Then, on the last Monday in March, President Trump hinted he might walk away from the conflict entirely. The S&P 500 surged 1.5%. The Nasdaq climbed nearly 2%. A few days earlier, markets had rocketed higher when Trump announced “productive” talks with Iranian representatives. A few days after that, stocks plunged again when he extended a deadline for Iranian compliance by ten days. Every pronouncement from the Oval Office has become a market-moving event — not because it changes anything about Google’s search revenue or NVIDIA’s GPU demand, but because traders are playing a game that has nothing to do with the companies they’re trading.

This is the market we’ve built: one where Brent crude’s 60% monthly surge matters more than NVIDIA’s 73% revenue growth; where the Strait of Hormuz has more influence over Apple’s share price than the iPhone’s installed base; where a presidential Truth Social post at 6 a.m. can swing the Dow by 500 points before most Americans have brushed their teeth.

And who’s orchestrating this symphony of irrationality? Not the retail investor with $5,000 in a Robinhood account. The institutional machinery — the hedge funds, the multi-manager platforms, the algorithmic traders — sets the tempo.

Firms like Citadel, which manages over $65 billion in assets and whose subsidiary Citadel Securities handles roughly 25% of all U.S. equity trades, exist in a universe so far removed from the average 401(k) holder that they might as well be playing a different sport entirely. Citadel alone added $2.52 billion to its Amazon position and doubled its NVIDIA stake in early 2026, moves that signal conviction in long-term fundamentals — even as the firm’s broader trading strategies profit from the very volatility that punishes everyone else.

The “Great Rotation” of 2026 tells the whole story. Approximately 45% of institutional investors are boosting hedge fund allocations this year. Retail investors, meanwhile, are injecting capital at twice the five-year average — buying dips that institutions are selling. JPMorgan’s own quantitative analysts have documented this divergence. The institutions rotate into energy, industrials, and alternatives. Retail holds the bag. The ball pit is not an equal-opportunity playground.

Hedge funds hedged 60-80% of their Magnificent 7 positions through puts, index shorts, and derivatives, creating asymmetric payoffs that retail investors simply cannot replicate. When NVIDIA drops 5% on a stellar earnings report, it’s not because the company failed. It’s because someone, somewhere, needed the stock to move in that direction for their derivative position to print.

The stock market isn’t broken — it’s working exactly as designed. The design just doesn’t include you.

Here is what we know to be true as of April 2026: Alphabet is on pace for another year of accelerating revenue, with Cloud alone on a $70 billion annual run rate and a $240 billion backlog. NVIDIA’s forward guidance implies it will generate more revenue in a single quarter than most Fortune 500 companies earn in a year. These are not struggling businesses. They are profit-generating machines of historic proportion.

And yet every one of their stocks is underwater this year, not because the numbers are wrong, but because the game is rigged toward those who trade the news, not the fundamentals. A president wages war and tweets about it. Hedge funds rotate billions in and out of positions overnight. Oil prices spike and suddenly Google’s advertising business is worth 15% less, for reasons that would make a first-year economics student laugh.

The Magnificent 7’s fundamentals remain magnificent.

The market’s response to those fundamentals is the tantrum of a toddler in a ball pit — chaotic, irrational, and utterly indifferent to the mess it leaves behind for the rest of us to clean up.

The balls keep flying. The children keep playing. And somewhere, a retail investor checks their portfolio, sees another red day, and wonders why the best companies on Earth can’t seem to catch a break.

The answer, of course, is that nobody on Wall Street is trying to give them one.